CD Calculator - Certificate of Deposit Estimator

Certificate‑of‑Deposit Calculator

For illustrative purposes only. Actual CD terms, penalties, and APY may vary by institution.

Growth Visualization

How to Use Our CD Calculator: A Complete Guide

Welcome to our comprehensive CD compound interest calculator, designed to help you understand exactly how much your Certificate of Deposit will earn. Whether you're looking for a CD calculator compounded monthly or daily, our tool provides accurate calculations for all compounding frequencies.

Understanding CD Interest Calculations

Our normal CD calculator helps you determine the potential earnings of your Certificate of Deposit investment. Unlike basic savings accounts, CDs offer guaranteed returns through fixed interest rates and various compounding options. Here's how to calculate CD interest effectively:

Example Calculation

In this example:

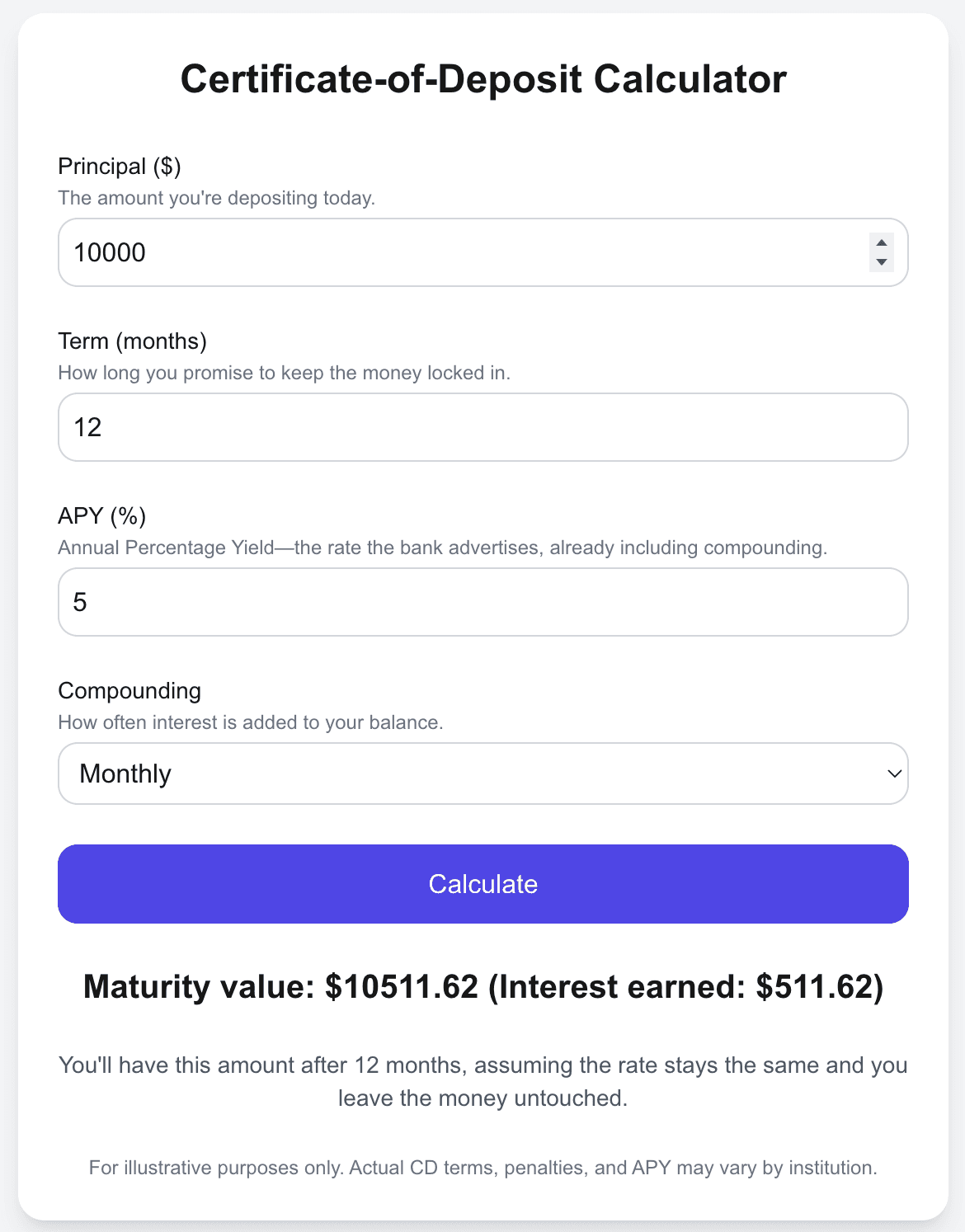

- Initial Deposit: $10,000

- Term: 12 months

- APY: 5%

- Compounding: Monthly

- Final Value: $10,511.62

- Interest Earned: $511.62

The graph shows how your balance grows steadily over the 12-month period, with each monthly compound increasing your earnings.

- Initial Deposit: Enter your principal amount - this is the money you'll lock away in your CD.

- Term Length: Specify how long you'll keep your money in the CD.

- APY (Annual Percentage Yield): Input the offered APY, which accounts for compound interest effects.

- Compounding Frequency: Choose between daily, monthly, quarterly, or annual compounding.

Advanced Features and Calculations

Whether you're considering a Wells Fargo CD or exploring other institutions' offerings, our calculator helps you compare options effectively. The CD compound interest calculator takes into account:

- Compound Interest Effects: See how different compounding frequencies affect your final earnings.

- APY Comparisons: Compare various CD rates to find the most profitable option.

- Total Returns: View both your initial investment and earned interest separately.

- Early Withdrawal Impact: Understand potential penalties for early withdrawal.

Making the Most of Your CD Investment

To maximize your CD earnings, consider these expert strategies:

- Compare Compounding Frequencies: Use our CD calculator compounded daily feature to see how more frequent compounding increases your returns.

- Understand APY vs. Interest Rate: Focus on the APY for true earnings comparison between different CDs.

- Consider CD Laddering: Explore creating a CD ladder for better liquidity while maintaining higher yields.

- Watch for Promotional Rates: Many banks offer special CD rates for new customers or larger deposits.

Why Choose Our Calculator

Our CD calculator stands out because it:

- Provides instant, accurate calculations for any CD term and amount

- Offers flexible compounding options (daily, monthly, quarterly, annually)

- Shows detailed breakdowns of interest earned and final balances

- Helps compare different CD options to maximize your returns

- Includes educational resources and expert tips for CD investing

Pro Tip: Understanding CD APY

When comparing CDs, always look at the APY rather than the simple interest rate. The APY accounts for compounding frequency and gives you the true annual return on your investment. Use our calculator's APY feature to make informed decisions about your CD investments.

CD Calculator FAQ – Top 10 Certificate of Deposit Questions

1. What is a Certificate of Deposit (CD)?

A CD is a time deposit offered by banks and credit unions. You agree to keep your money on deposit for a set term—in return, the institution pays a fixed interest rate that's usually higher than a regular savings account.

2. How is APY different from interest rate?

The Annual Percentage Yield (APY) includes the effect of compounding, while the nominal interest rate does not. Our CD calculator uses APY so you see the true yearly return.

3. What happens if I withdraw money before the CD matures?

You'll pay an early‑withdrawal penalty, typically a few months of interest. Always check the bank's disclosure before opening a CD.

4. Are CD rates fixed for the entire term?

Yes—traditional CDs lock in a fixed rate until maturity, protecting you if market rates fall but preventing gains if they rise.

5. How often do CDs compound interest?

Compounding frequency varies by institution—common options are monthly, daily or annually. More frequent compounding yields slightly higher returns.

6. What is a "no‑penalty" CD?

A no‑penalty CD lets you withdraw your full balance after a short lock‑up (e.g., 7 days) without paying the usual early‑withdrawal fee. Rates are usually a bit lower to compensate.

7. Are CDs FDIC or NCUA insured?

Yes—up to $250,000 per depositor, per bank, CDs are insured by the FDIC (or NCUA for credit unions), making them one of the safest fixed‑income investments.

8. How are CD earnings taxed?

Interest earned on CDs is taxed as ordinary income in the year it's credited—even if you leave the interest inside the CD until maturity.

9. What is a CD ladder and how does it work?

A CD ladder splits your money across multiple CDs with staggered maturities (e.g., 1‑, 2‑, 3‑, 4‑, 5‑year). One CD matures every year, giving you regular access to cash while still locking most funds into higher long‑term rates. Learn more about jumbo CD ladders.

10. CD vs. high‑yield savings account: which is better?

High‑yield savings accounts offer rate flexibility and instant access, but the rate can drop at any time. CDs lock in a guaranteed return but tie up your funds. Use our CD calculator to compare today's high‑yield CD rates against your savings account APY.